Intel Q2 2014 Quarterly Earnings Analysis

by Brett Howse on July 15, 2014 7:55 PM EST- Posted in

- Intel

- Smartphones

- Mobile

- Datacenter

- desktops

- Notebooks

On July 15, Intel released their Q2 2014 Earnings report for the period ending June 28, 2014.

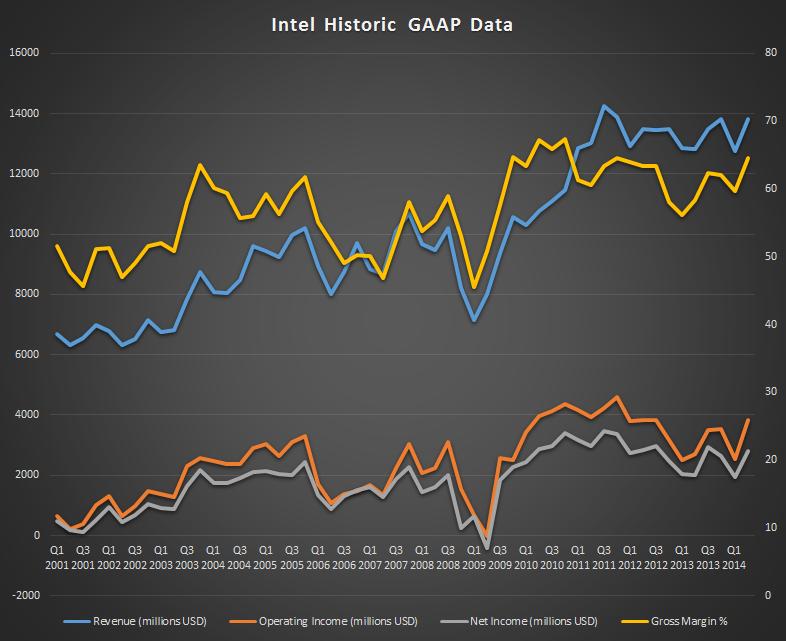

GAAP revenues for the quarter came in at $13.8B which is up almost a billion over Q1 2014, and also up a billion on Q2 2013 for a strong 8% increase.

Earnings Per Share was $0.55, up a substantial 41% year-over-year, and beating analysts’ expectations of 52 cents per share.

| Intel Q2 2014 Financial Results (GAAP) | |||||

| Q2'2014 | Q1'2014 | Q2'2013 | |||

| Revenue | $13.831B | $12.764B | $12.811 | ||

| Operating Income | $3.844B | $2.533B | $2.719B | ||

| Net Income | $2.796B | $1.947B | $2.000B | ||

| Gross Margin | 64.5% | 59.7% | 58.3% | ||

| PC Group Revenue | $8.7B | +9% | +6% | ||

| Data Center Group Revenue | $3.5B | +14% | +19% | ||

| Internet of Things Revenue | $539M | +12% | +24% | ||

| Mobile Group Revenue | $51M | -67% | -83% | ||

| Software and Services Revenue | $548M | -1% | +3% | ||

| All Other Revenue | $517M | -5% | +16% | ||

The stagnant PC sector is finally showing some signs of life again after declining over the last several years. Intel’s PC Client Group reported revenue of $8.7 billion, up 9% over last quarter and 6% year-over-year. Unit volumes of PC Client chips were up 12% over last quarter, and 9% from last year. The average selling prices (ASP) were down 3% from Q1 2014 and 4% from Q2 2013. Most of this can be attributed to a 7% drop in ASP for the notebook platform, where as desktop chips actually slightly increased ASP over Q2 2013.

Data Center revenue was up an even more impressive 19% over Q2 2013, and 14% over last quarter. Data Center volumes were up exactly the same as the PC Client volumes – 12% over the previous quarter and 9% over the previous year, but ASP for the Data Center platforms was up 3% over Q1 2014 and 11% over Q2 2014.

The recently formed “Internet of Things” group continued its strong growth, up again another 12% over last quarter and 24% year-over-year. This group includes embedded segments such as retail, transportation, and consumer focused things like home automation.

The one sector at Intel which continues to struggle is the Mobile and Communications group which was down 61% Q1 2014 versus Q1 2013, and once again in Q2 2014 it was down again 67% compared to Q1 and 83% year-over-year. The silver lining on this is the relatively small amount of revenue this is for Intel with this group only having $51 million in revenue, but in a world where the number of mobile devices is skyrocketing, Intel is struggling to capitalize on the new market. Intel is still not price competitive with the Bay Trail SoC business and are working on a low cost platform for Bay Trail. In the meantime, Intel is subsidizing the platform cost for the time being in order to not be shut out of this market. It’s not something that would be sustainable forever, but it seems to be allowing them a toehold in the mobile market while they continue to push towards lower cost silicon for partners. We’ve seen a lot of mobile devices coming with Bay Trail in the last couple of months, including a $110 Toshiba tablet and this contra revenue is driving that, but hurting the short term results for the Mobile group.

The last sector at Intel to report was the Software and Services, coming in at $548 million in revenue which is pretty much flat quarter-over-quarter and year-over-year. This segment includes McAfee which was purchased by Intel in the not so distant past.

The forecast for next quarter and the rest of the year has been upgraded, with Q3 2014 being forecast for $14.4 billion plus or minus $500 million. The board has also approved an additional $20 billion in share repurchases, with an expectation of $4 billion in shares to be repurchased in Q3. Looking back historically, Intel is once again getting close to record revenue and incomes, having almost fully recovered to 2012 levels.

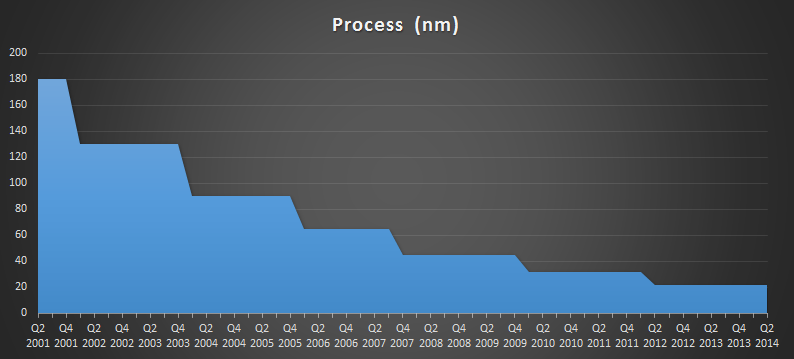

Broadwell is now expected during the holiday season 2014, which is certainly much later than hoped. Going back to 130 nm and coming forward until 32 nm, Intel has averaged 8.2 quarters between process nodes. They have been on 22 nm for nine quarters already, meaning the wait between 22 nm and 14 nm will be about 11 quarters which will be the longest time on a single process node since Intel began the tick tock strategy. Clearly there are some heavy engineering hurdles to overcome as we move towards smaller and smaller processes. We’ll have to watch and see if this delays Skylake or if Broadwell has a shorter than expected lifespan. 10 nm is on the roadmap for 2016 which might be an aggressive timeline with the time 14 nm has taken.

This was a great quarter for Intel, which is generally a bellwether for the rest of the PC industry. After several years of decline, things are looking more optimistic for the industry. Revenues from Intel were great, but historically they have always done well. The exciting takeaway from this earnings report is the increased volumes in both notebook and desktop sales. Whether this is a turnaround in the market, or just a small correction is tough to tell yet.

Source: Intel

33 Comments

View All Comments

skiboysteve - Tuesday, July 15, 2014 - link

1) wow what a great quarter for Intel! All the cloud services are really helping them sell data center stuff2) why the hell did they buy McAfee?

Kevin G - Wednesday, July 16, 2014 - link

This is Intel's first full quarter with Ivy Bridge-EX out on the market. A lot of companies have been waiting for this chip as it brings a new platform (remember there was no Sandy Bridge-EX). I know of companies who are still using Nehalem-EX servers in production and looking to replace them after 4 years of good service.Enterprise storage and networking are also doing pretty well for Intel.

The future is bright in this area with some revolutionary technologies like silicon photonics on the horizon.

The only real enemy in this space isn't a hardware competitor but rather crazy software licensing as socket, core and memory count increases. The hardware is good but if companies can't afford to run their software on it, demand will flat line over the long term. I expect Intel to become more involved in some open source projects as a message to several key enterprise developers.

eanazag - Wednesday, July 16, 2014 - link

They bought McAffee because they wanted/needed software to go with new security features in hardware. The problem is that they bought McAffee and not someone who could innovate. Software that went hand in hand for managing encryption on their SSDs, took advantage of their AES instructions to encrypt drives that are missing hardware based encryption. They should have bought Symantec. I don't think Symantec's software is great, but they do execute.and their software is decent. Intel should have bought Nvidia when AMD bought ATI. They've wasted a lot of money developing GPU hardware and software assets.The problem with buying Symantec and Nvidia is the cost. Actually, buying Nvidia now makes more sense than ever before. They have a better mobile business than Intel (chips and modems), obviously GPUs, enterprise GPUs, CUDA, and software assets. And they had a great chipset business till Intel and AMD forced them out. Intel made a huge mistake by not letting Nvidia get an x86 development license; they forced them into the ARM camp.

sonicmerlin - Wednesday, July 16, 2014 - link

Uh... Intel can't buy nvidia, as the purchase would be shot down by antitrust authorities. It's kind of hard to take the rest of your comment seriously when you don't even realize that much.name99 - Wednesday, July 16, 2014 - link

"All the cloud services are really helping them sell data center stuff"It remains to be seen how sustainable this is. Intel have had no serious competition in the data center for years. POWER and Oracle/Sun are specialized (and expensive) tastes, AMD burns too much power, ARM has been limited to 32 bit.

Over the next year the ARM story changes, with 64-bit available, the LAMP stack becomes standardized thanks to Linaro, and the ARM server spec becoming standardized. A57 should be, for most purposes good enough in latency (ie single-threaded throughput) but with the ability to run mass throughput at lower power and substantially lower cost than Xeon.

Intel may try to fight back by dramatically lowering the cost of Xeons, but while that may stave off ARM in the datacenter, it won't help sustain their revenue.

sonicmerlin - Wednesday, July 16, 2014 - link

Data centers want higher IPC. They don't want to deploy 10x as many servers, even if the overall TDP of ARM is better, because there are large costs associated with housing and maintaining each and every server. As long as Intel leads in IPC they'll never need to lower Xeon prices.przemo_li - Monday, July 21, 2014 - link

More than 50% of costs for data centers come from POWER usage.So no, neither IPC, nor power usage counts.

Power efficiency (how much we can do with given power budget) matter.

And if ARM SoCs offer improvements, without disruption, then they will be choosen over Intel offering in the blink of the eye.

Only saving grace Intel have currently is software support. And not "end-user software" as that is gcc recompile away (as it should be!), but firmware/drivers mess current "embeded" ARM OEMs create.

You can grab Intel source code, heck You do not even have to. Just Linux kernel (Intel code is included after all), compile it, slap into Your distro of choice, and You are ready.

With ARM You need those release-once-forget-about-customers-after-that binary blobs.

AMD went so far as to OpenSource their gaming GPU business for the sake of servers. ARM crowd laggs behind seriously.

Lack of flexibility -> higher costs of maintaining & less innovation.

jobo32 - Thursday, July 17, 2014 - link

I wonder if other companies besides Microsoft will start looking into FPGAs to get several times faster performance. Microsoft claimed to get 10x better performance for their FPGA based Catapult projectprzemo_li - Monday, July 21, 2014 - link

Intel is integrating some FPGA's in their server lineup.So everybody will be able to try their luck with them.

TheJian - Tuesday, July 15, 2014 - link

So mobile revenue of about 50mil but losing a billion on it. So basically you are completely GIVING these away to sell them...LOL. Quit and your earnings go up a full billion dollars.Why does anandtech tell revenue instead of EARNINGS from each dept? Or heck better yet post BOTH. Intel paying you to NOT say how much mobile is losing (950mil last quarter)? Otherwise why leave out that VERY important detail to shareholders who say they should just give it up (many analysts say this). Not expected to put out anything decent on mobile until 2016 really and the competition won't sit still. We keep hearing, the next rev will do it...ROFL. Now they've given up that and say two revs it will happen (or more depending on who you believe).

By NV or give up mobile. Now that would be a HUGE game changer especially with Intel's process. Can you imagine qcom trying to keep up with a 14nm K1 Denver? Intel wouldn't have to GIVE these away, they'd sell themselves. Pay whatever Jen Hsun needs to leave or merge (a few billion on top of the buy price in a personal check should do it) and be done with it. Imagine the 14nm gpus coming out too. Again total dominance in mobile and gpu for a long time if they pump out 14nm NV stuff while owning them. Also I'm sure they'll be able to sue qcom at some point as IMHO they hide their gpu tech from everyone because they are stealing tech they should be paying for (or why hide while everyone else shows the cards?). Nobody is really using fancy tricks these days (which is why amd/nv basically tie each gen now), so what is qcom hiding? Intel would have the money and lawyers to take qcom down a notch at some point.

NV is the only way to stop the ARM juggernaut (if you can't beat them join then right?). Make a move Intel before arm enters desktops and takes 21% of that just like they did notebooks already. With android L and 64bit they can move to desktop for at least a decent portion of users who don't do much more than browse, email and casual gaming. That describes a LOT of users.

I don't believe the bump for intel will last long, it mainly happened because of xp dying via MS support. Companies were forced to look forward more.